Ag futures. The movements of a few other commodity and financial futures prices are frequently used by market analysts and traders to explain near term movements in ICE cotton futures. CBOT corn and soybean futures might be expected to move similarly with ICE cotton in that these are competing row crops for land. This is typically expressed in the business press as “outside markets were supportive (or not) for cotton”, referring to higher (or lower) grain and oilseed prices. But it may be more complicated than that. Cotton, corn, soybeans, and wheat are all globally traded commodities, and sometimes one crop will be affected by bullish/bearish news that is independent of other agricultural commodities. For the week ending Thursday, October 9, CBOT corn and KC wheat futures both gyrated up and down, ending the week in an extended down trend. CBOT soybeans trended higher before switching to a dowon trend.

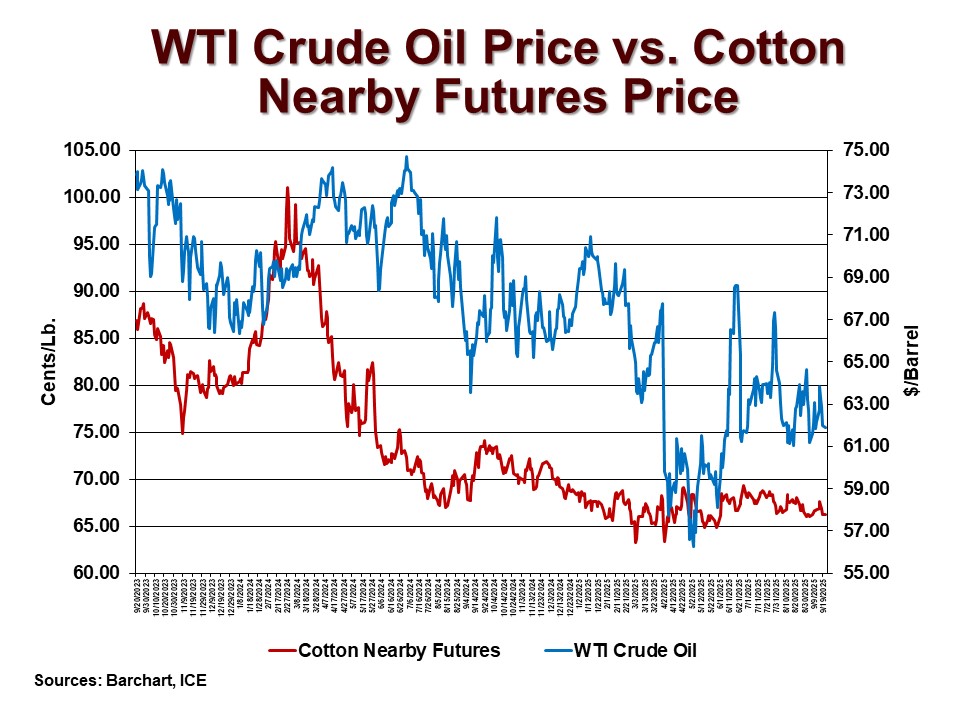

Other commodities. Crude oil futures prices (e.g., ICE WTI) are often assumed to be negatively correlated with ICE cotton because crude oil distillates are used to manufacture polyester, a rival fiber to cotton. It is a common explanation in the business press that, for example, “…rising (or falling) cotton prices this week were influenced by weaker (or stronger) crude oil prices…”. But again, the story is probably more complicated, as described in this economic study. For example, oil and cotton futures may rise together if such behavior is in response to a booming economy. Also, rising oil prices are associated with more expensive diesel fuel, which increases the cost of producing crops, which could be inflationary. For what it’s worth, the last two years of WTI oil and ICE cotton futures appear to have a longer term co-movement, perhaps being similarly affected by covid, stimulus, and post-stimulus hangover. For the week ending October 9, ICE WTI crude oil futures started the week flat-to-higher before switching into a descent (see lower right chart courtesy of Barchart.com).

Currency futures. It is often assumed that ICE cotton futures move the opposite of the value of the U.S. dollar (as measured by the ICE dollar index). The fundamental reason for this is that a weaker dollar relative to, say, the Brazilan real, makes U.S. cotton (and corn, soybeans, etc.) exports less expensive than Brazilian exports of those commodities. Further, the value of the U.S. dollar relative to other currencies might also partially explain speculative influence on cotton prices. As the U.S. dollar weakens, it can encourage flows of money into alternative financial markets like commodity futures. In addition, a weakening U.S. dollar in theory would stimulate more U.S. exports of physical cotton since it would be cheaper relative to competing foreign cotton. So there is a double reason for cotton markets to get stronger when the U.S. dollar weakens, and vice versa. The weak dollar/stronger cotton price relationship has generally been the case except during very specific situations like a sustained weakening euro currency (e.g., late 2009/early 2010, and again in late 2011). Through October 10, the U.S. Dollar Index ascended and leveled off on Friday (see chart below courtesy of Barchart.com).